UP: Earnings Up Despite ‘Tough’ 2Q22 (UPDATED, Cowen)

Written by Marybeth Luczak, Executive Editor

(Photograph Courtesy of UP)

“As anticipated, the second quarter was a tough one as we limited carloadings and increased expenses to recover network fluidity,” Union Pacific (UP) Chairman, President and CEO Lance Fritz reported during a July 21 earnings announcement. “We also experienced record high fuel prices and increasing inflation, adding pressure to our total costs. Offsetting the cost pressures were higher fuel surcharge revenue, solid core pricing, a positive mix, and continued train-size initiatives. The result was operating revenue and income growth.”

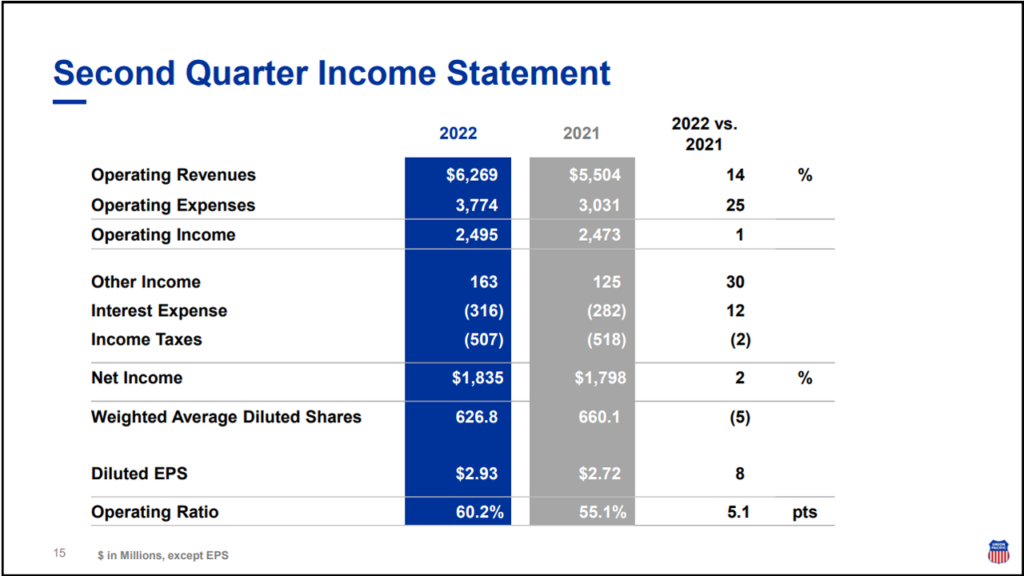

UP posted second-quarter 2022 net income of $1.835 billion (or $2.93 per diluted share), up 2% from prior-year period’s $1.798 billion (or $2.72 per diluted share).

Among the Class I railroad’s other second-quarter 2022 results:

• Operating revenue of $6.269 billion was up 14% from second-quarter 2021’s $5.504 billion, “driven by higher fuel-surcharge revenue, core pricing gains, and a positive business mix, offset slightly by volume declines,” according to UP.

• Business volumes, as measured by total revenue carloads, were down 1% from second-quarter 2021.

• The 60.2% operating ratio deteriorated by 510 basis points over the prior-year period, according to UP, which noted that “higher fuel prices negatively impacted the operating ratio 130 basis points.”

• Operating income of $2.495 billion was up 1% from second-quarter 2021’s $2.473 billion.

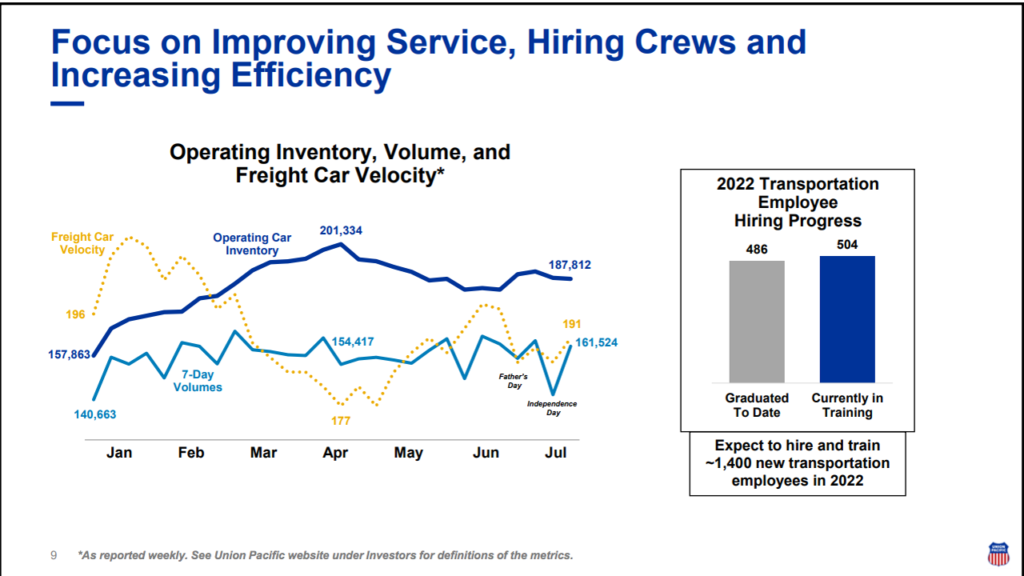

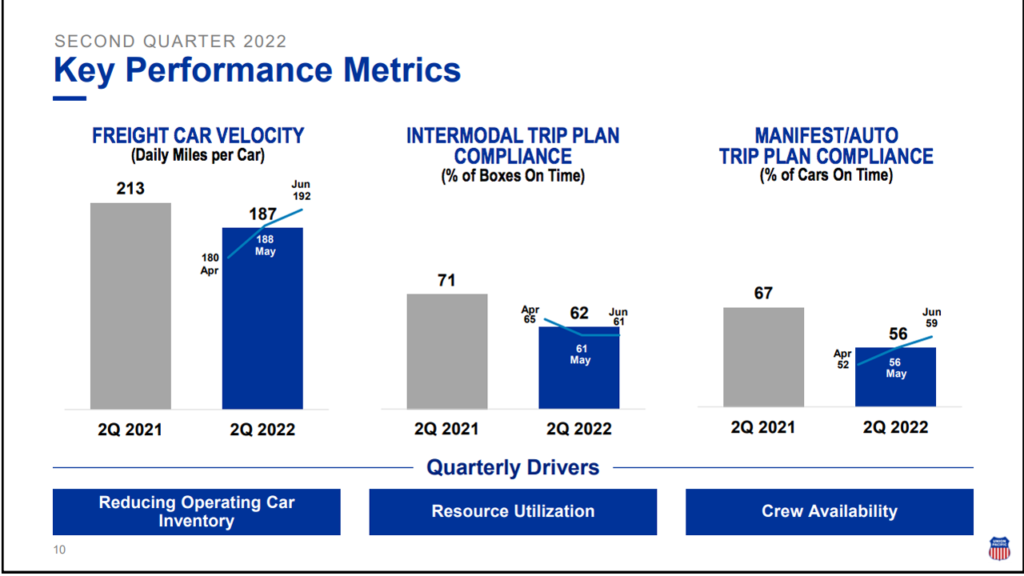

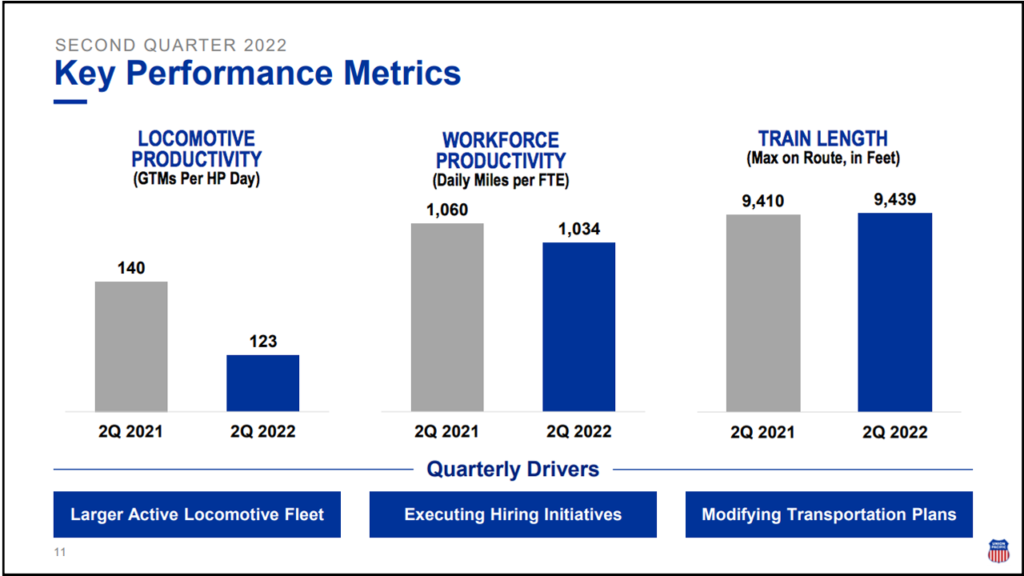

In terms of operating performance, UP reported a 12% decline in both quarterly freight car velocity (187 daily miles per car) and quarterly locomotive productivity (123 gross ton-miles/GTMs per horsepower day) from the prior-year period. Average maximum train length was flat at 9,439 feet. Additionally, quarterly workforce productivity was 1,034 car miles per employee, a 2% decline from second-quarter 2021, and the fuel consumption rate of 1.076 (measured in gallons of fuel per thousand GTMs) was flat. UP said its first-half reportable personal injury rate improved to 0.93 per 200,000 employee-hours compared with 0.95 for first-half 2021.

2022 Outlook

Since “first-half 2022 results challenge previous full-year volume and operating ratio targets,” UP said, it provided these updates:

• “Stronger second-half volumes should produce full-year carload growth of 4% to 5%.

• “Full-year operating ratio of around 58%.

• “Second-half operating ratio improvement vs. 2021.

• “Second-half incremental margins around 50%.”

The railroad affirmed for 2022 pricing gains “in excess of inflation dollars”; capital spending of $3.3 billion; long-term dividend payout target of 45% of earnings; and share repurchases “in line with 2021.”

The Cowen Insight: ‘Navigating Windy Tracks’

“UP came in above expectations in the second quarter despite significant network challenges, as anticipated,” reported Cowen and Company Managing Director and Railway Age Wall Street Contributing Editor Jason Seidl. “Second-half guidance suggests a noteworthy turnaround in operations that we remain cautious on, given no significant volume improvements quarter-to-date. Demand was left on the table in the second quarter, while UP ramps hiring to improve service metrics. PT to $261 and reiterate Outperform.”

Key Cowen Takeaways:

• “Second-quarter adjusted EPS of $2.93 came in above our $2.83 forecast and the consensus estimate of $2.86. Operating ratio (OR) of 60.2% missed our 57.4% forecast, worsening 510bps year-over-year, driven by fuel surcharges (even without a recovery lag there would be an OR hit) and network recovery challenges. Despite pressure on OR in the quarter, UP appeared to lean into pricing again to drive growth in the quarter.

• “Second-quarter volumes declined 1%; the decline was led by intermodal, which fell 8%, followed by grain (–4%). Domestic intermodal appears to have both network challenges and a demand pullback as truck spot rates have come down materially. International intermodal should largely be driven by the global supply chain fluidity and changes to China’s COVID shutdowns. Automotive volumes improved 11% as strong demand is driven by the easing of semiconductor supply and pent-up demand. Management sees full-year volume growth between 4%-5%, which would imply a significant ramp (high single digits) for the remainder of the year. Our rail-share data suggests that UP volumes are +1% quarter-to-date, which is below management’s targets. We don’t expect rail fluidity to improve as quickly and therefore volumes expectations seem lofty; we have chosen to model slightly below the low end of management’s volume guidance.

• “Year-to-date, UP has brought on 486 employees and currently has 504 in training, with approximately 400 of those coming into the network by the end of the third quarter. Workforce productivity declined 2% in the quarter as car miles were flat, despite an increased employee count. We hope that as employees ramp (which industry panelists on previous calls we have hosted stated can take approximately three-to-six months before a new rail employee is ramped and productive) that productivity metrics begin surfacing and improved service metrics follow.

• “Management expects adjusted OR for the full year at approximately 58% after the 60.2% in the second quarter and 59.4% in the first quarter. While we do expect OR to improve in the second half, UP has already increased (worsened) their 2022 OR guidance twice this year, and we see a scenario where this could happen again if conditions to not improve materially. We are cautiously optimistic, though model our full year OR 60bps above (worse than) management’s updated guidance (similar to our revenue forecast). Fuel will be a large picture to this cadence, which will likely continue to be volatile and detrimental to OR.

• “Given the second-quarter earnings beat, we increase our 2022 EPS estimate to $11.70 from $11.62, while maintaining our 2023 EPS estimate of $12.75. Given the duration of network challenges, uncertain macro outlook, and unconvincing second-half outlook, we lower our multiple two turns (similar to our CSX multiple adjustment) to 20.5x (this moves UP’s multiple more toward its historical average). Using our new 20.5x multiple and our intact 2023 EPS estimate, our price target goes to $261. Reiterate Outperform.”