Commentary

REF 2023: The Intermodal Environment

Written by Ron Sucik, Contributing Editor and Principal, RSE Consulting

BNSF Logistics Park Kansas City. BNSF photo

RAIL EQUIPMENT FINANCE 2023: Last October, the Wall Street Journal declared the ship backlog at the Port of Los Angeles/Long Beach (POLALB) to be over, providing three reasons:

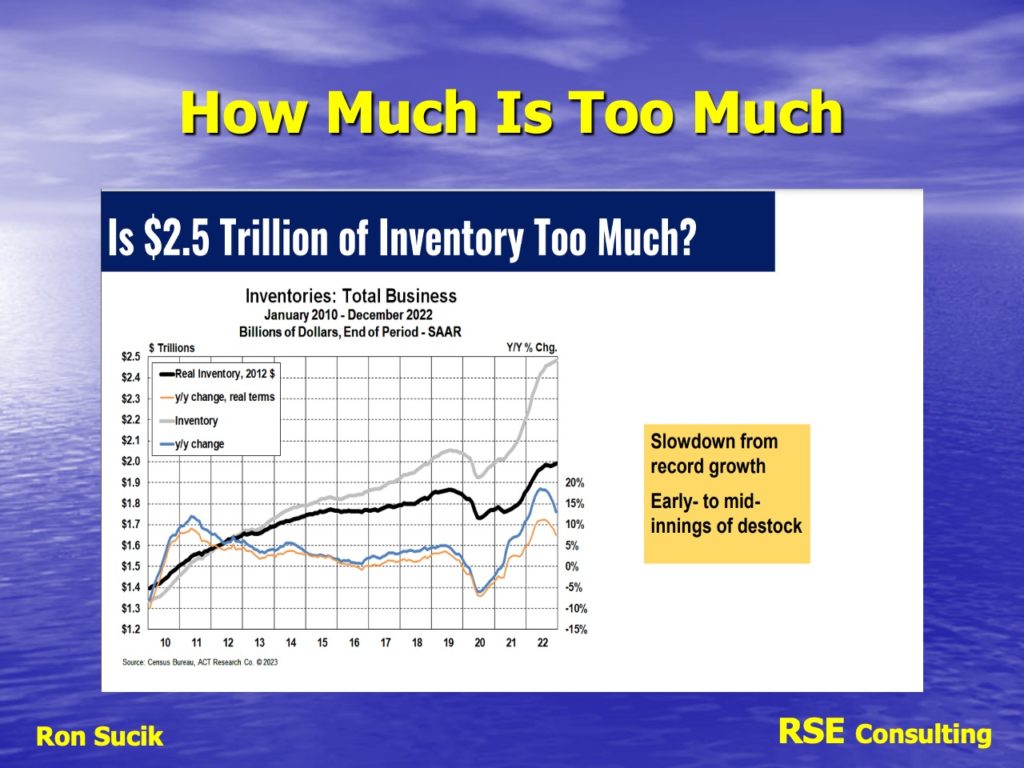

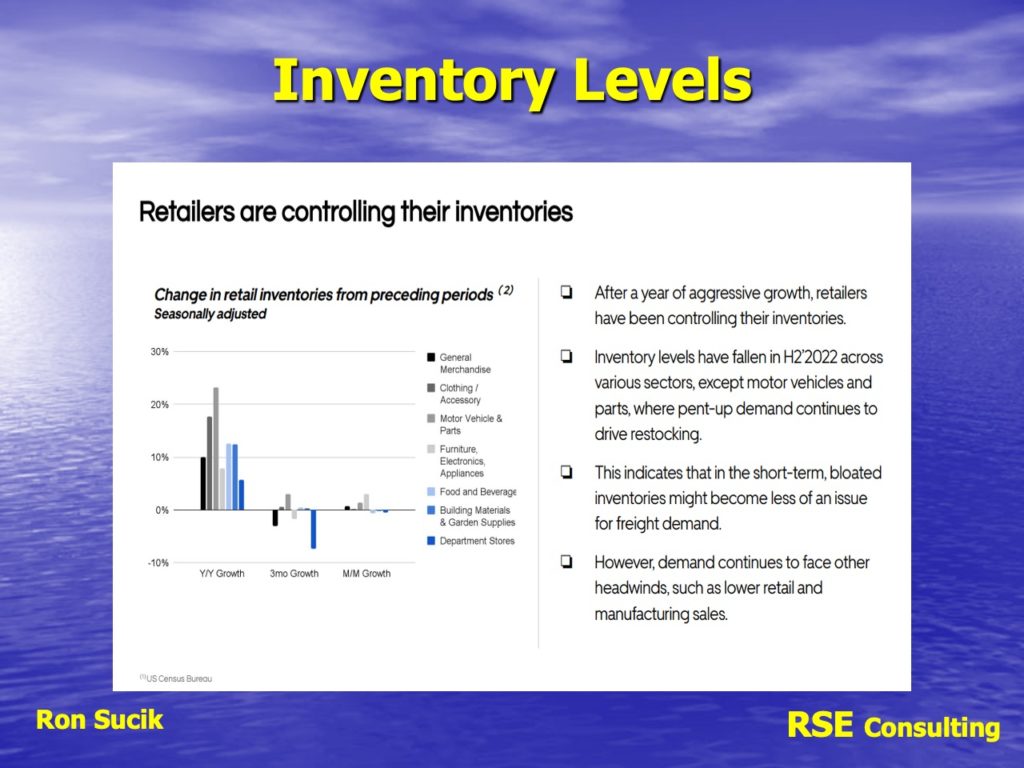

- A substantial increase in inventory as a result of overordering by merchants, a pattern of behavior that went back to early 2002, leading to widespread retail discounting and oversupply.

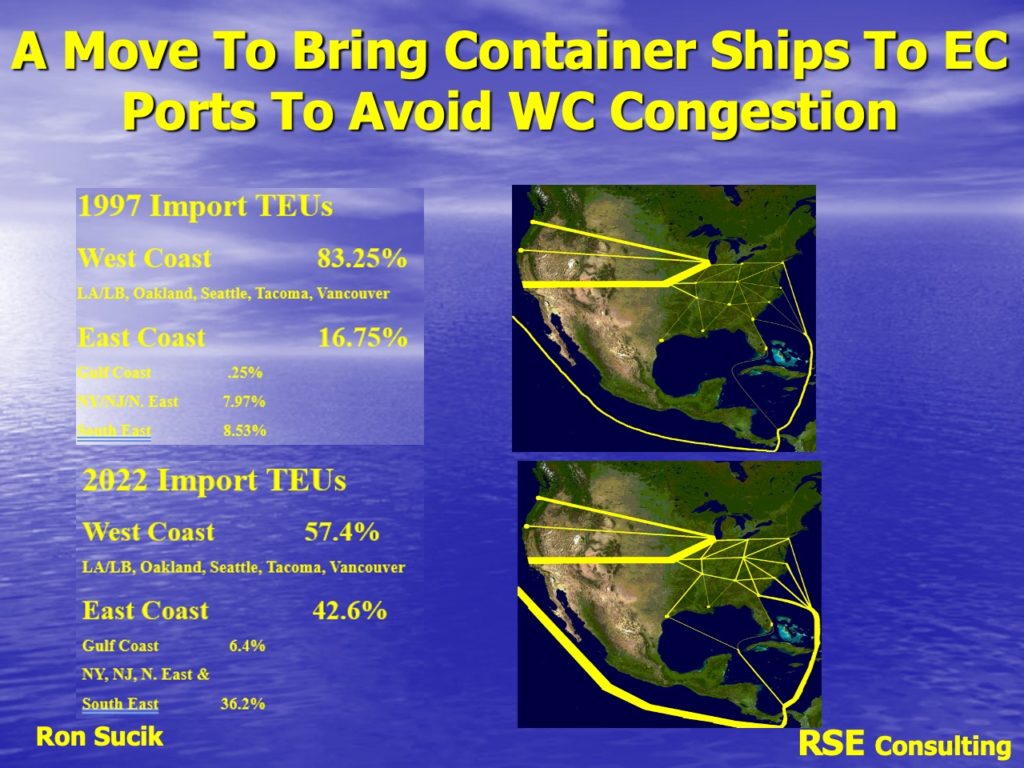

- A move to bring container ships to East Coast ports to avoid West Coast congestion.

- Concerns about an impending ILWU (Longshoreman) strike—which also resulted in a move of more ships to the East Coast.

When traffic bogged down and manufacturers were locked out in China, some retailers engaged in “panic buying” and ordered anything they could get their hands on. This mix of products bogged down the warehouses trying to move the inventory, making it especially difficult to distribute the correct seasonal products.

Many ISO containers arriving at the port were immediately stacked and often did not move first-in, first-out. Often, the last container in was the first out. This further mixed the products moved to the warehouses for transloading and distribution. This difficulty for the retailers to sort and distribute the correct products resulted in many loads remaining on chassis in their yards, also resulting in shortages of chassis in terminals to move these ISO containers. Turn times on chassis climbed to 10 days, when the average should have been four. As the congestion and slowdown in consumer spending occurred, Amazon and Walmart cancelled $200-$300 billion of orders for 2023 as demand softened.

When I started trade flow studies in 1997, 83% of container traffic coming from Asia (China, Korea, Japan and Thailand) was discharged on the West Coast (primarily POLALB), while only 17% went through the Panama Canal or Suez Canal to East Coast ports.

The congestion and backup occurred for various reasons identified the past year:

- A depleted work force because of the pandemic or COVID Stimulus Checks.

- A surge of products.

- A poor seasonal mix of products sitting on chassis at warehouses, resulting in chassis shortages not only at the ports but also at inland rail terminals.

- Various railroad congestion and movement issues.

All of these resulted in the backup at West Coast ports, with more than 100 ships at berth or waiting at one time at the POLALB.

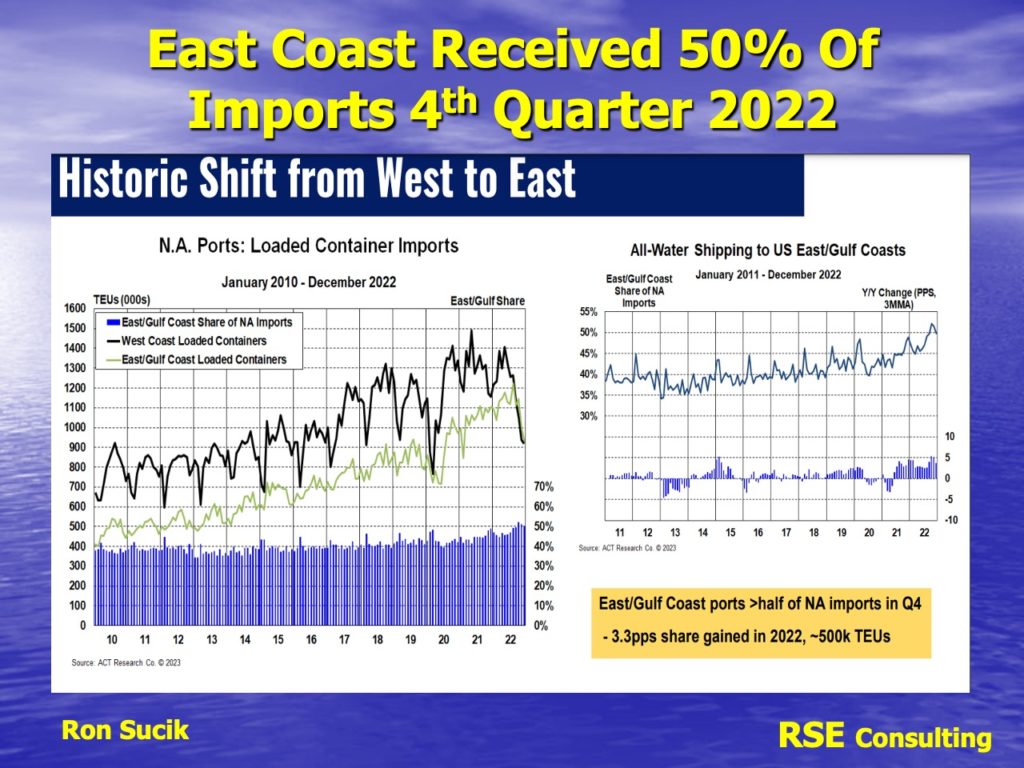

For years there has been a gradual shift of traffic as more retailers opened warehouses and distribution centers on the East Coast. In 2019, it had shifted to 62% to the West Coast and 38% to the East Coast. But with this congestion, the shift accelerated, resulting in 57% to the West Coast and 43% to the East Coast for 2022. In fact, at the end of 2022, the East Coast percentage had reached 50%.

One of the graphs ACT Research released at its latest conference is a very good reference to the shift of 50% of container ships going to the East Coast. Some of this shift is also the result of relocating some product sourcing from Asia to the West.

The ILWU contract expired in June 2022, but there isn’t much concern now because steamship companies have made a lot of money and may be more willing to accept the union’s demands this time.

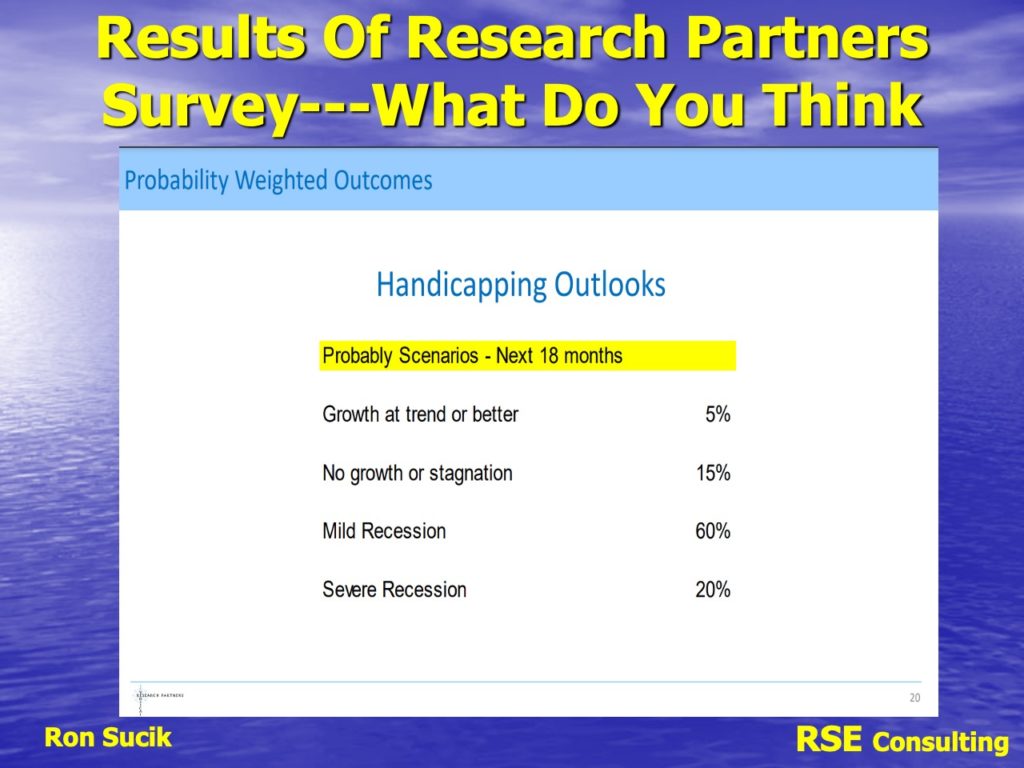

We didn’t attain the 5% growth that was predicted by the optimists last year. We couldn’t even get the 2.5% others predicted.

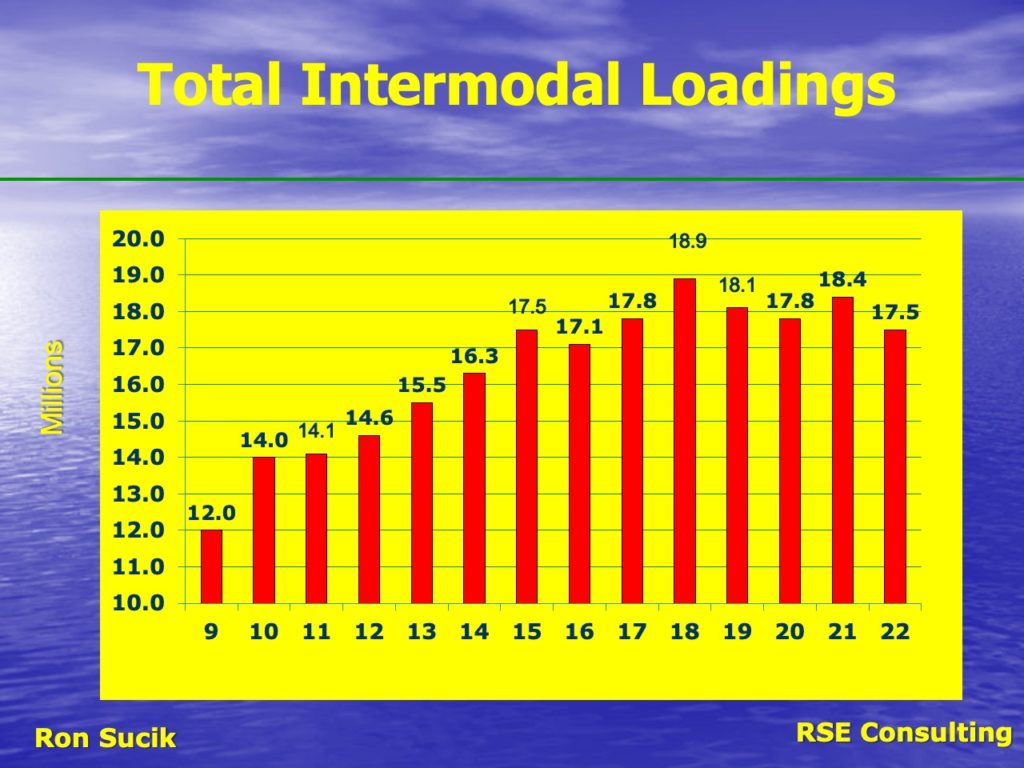

Intermodal loadings for 2022 were the sixth best, yet loadings were down 5% year-over-year, compared to 2021. Domestic container loading was down 1.8%; TOFC was down 23.87%. With early growth of 2.87% 2022’s first six months compared to the year-earlier period, imports declined 2% and ended up down 6% in 2022 after growing 5% in 2021. In fact, by the end of 2022, IPI (interior port intermodal) volumes were 7.5% lower than the pre-COVID levels of 2019. The scary thing is that intermodal has been forecasted by some to decrease another 5.1% in 2023.

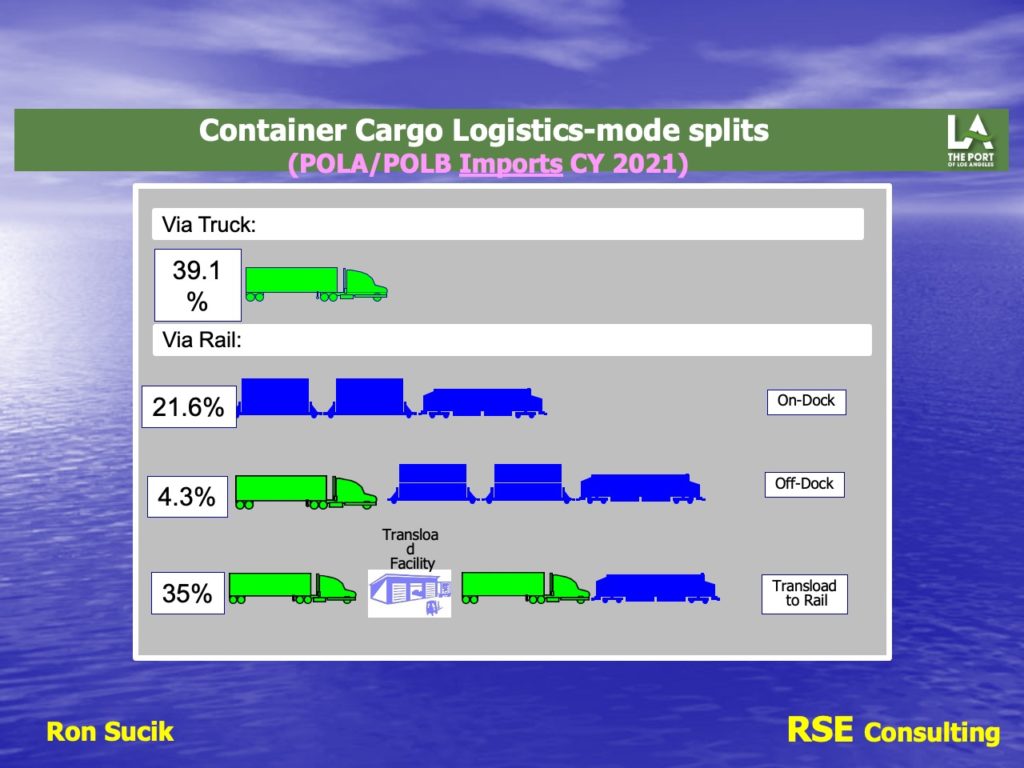

As information, the breakdown of arriving containers in 2021 at the Port of Los Angeles:

- 39.1% moved out of the port on OTR (over the road) trucks.

- 21.6% moved off the dock in an outbound train.

- 4.3% was loaded off-dock at railroad terminals.

- 35% went to a transload warehouse for resorting. This number reached into the high 40% during the congestion issues at the ports and on the railroads.

International Trade reported that many of Apple Inc’s Chinese suppliers are likely to move capacity out of the country far faster than many observers anticipate pre-empting fallout from escalating Beijing-Washington tensions. Nine out of 10 of Apple’s most important suppliers may be preparing a large-scale move to countries like India. Bloomberg Intelligence estimates it could take eight years to move just 10% of Apple’s capacity outside of China. However, a GoerTek executive argued it’ll be far quicker.

GoerTek Inc., which cranks out the bulk of the world’s gadgets from iPhones to PlayStations, is also exploring locations other than its native China. It’s investing an initial $280 million in a new Vietnam plant while considering an India expansion. Vietnam for now is the company’s sole manufacturing site outside of China. Many U.S. companies are planning to shift production there, regardless of cost.

Bloomberg Intelligence reported in December 2022 that a Deloitte survey of 305 executives at transport and manufacturing firms indicated 62% of manufacturers have started reshoring or near-shoring their production capacities. Ultimately, this shift could reduce share of Asia-originating shipments by 20% by 2025 and 40% by 2030. There are doubts it will return.

This month it cost $1,444 to ship a standard 40-foot ISO container from China to the U.S. West Coast—down from a peak of $9,682 in March 2022. Behind this fall is a decline in demand for goods, 90% which reach retailers by ship. Demand has plunged as inflation surged. The reopening of bars and restaurants and other facilities closed during the pandemic has led to more spending on service, as well. The fall in prices has been welcomed by importers, which are also having to adjust to reduced demand caused by the cost-of-living crisis.

Now for a downer: Last month, the IMF (International Monetary Fund) forecast that global trade growth would decline to 2.4% this year, from 5.4% in 2022.

Although December sales had tumbled 1.1%, January sales rose 3%. It marks the biggest monthly jump since March 2021. Food services and bars accounted for the biggest gain in January, with sales surging 7.2%.

I have heard stories that some retailers have seasonal product that arrived too late last year to be put into their stores, taking up space in their warehouses, resulting in fewer orders this spring. Other products are so mixed up from late arrivals and “panic buying,” and some are still sitting in containers in their yards. Retailers are having difficulty getting the right products to their stores at the right times.

By now you should have experienced some of the retail price reductions as they try to get rid of this surplus of old product. It is nothing to see 30% to 50% reductions on items, especially seasonal products.

Interestingly, a rancher friend in South Dakota called to tell me duck decoys that got into the local Walmart late were marked down 35%. Yet, I went looking for a pair of casual shoes at my local stores in Naperville, Ill., and although there were shoes, there weren’t any of the kind I wanted. Limited selections.

According to Drewry, 4.1% of the global container fleet was idled in February. This is the highest unused vessel capacity since a spike after the start of the pandemic. Spot container freight rates have fallen to their lowest level in two and a half years, and as previously mentioned, these prices are welcomed by the importers who are also having to adjust to reduced demand caused by the cost-of-living crisis.

You may see orders for 425 three-unit well cars in 2023. This represents 3,150 platforms of capacity capable of handling approximately 150,000 or more of new loadings growth. Motor carriers and logistics companies have added 30,000 to 35,000 new containers, bringing the number of domestic containers to more than 418,000 by the end of 2022. That represents 12% growth over 2021. This sets up a market with too much supply chasing not enough demand.

Chassis are still a challenge. Stoughton says that components and labor are still problems for their production.

In Barstow, Calif., about 120 miles from POLALB, BNSF will open the Barstow International Gateway, a new inland terminal scheduled for completion by 2027. This will allow BNSF to load IPI containers on dock at the ports and bring them to Barstow, where they will be either resorted for movement or unloaded for transloading or storage in the warehouses for later shipment. This is similar to the Inland Empire in Ontario, Calif.

JB Hunt has signed an intent to locate another onsite terminal at the facility. This could be similar to the four-corner transload facilities JBH has already created in Seattle, Commerce City, Savannah and New York/New Jersey. JBH personnel staff these facilities to handle import traffic because of the fear of congestion disabling existing facilities to handle imports.

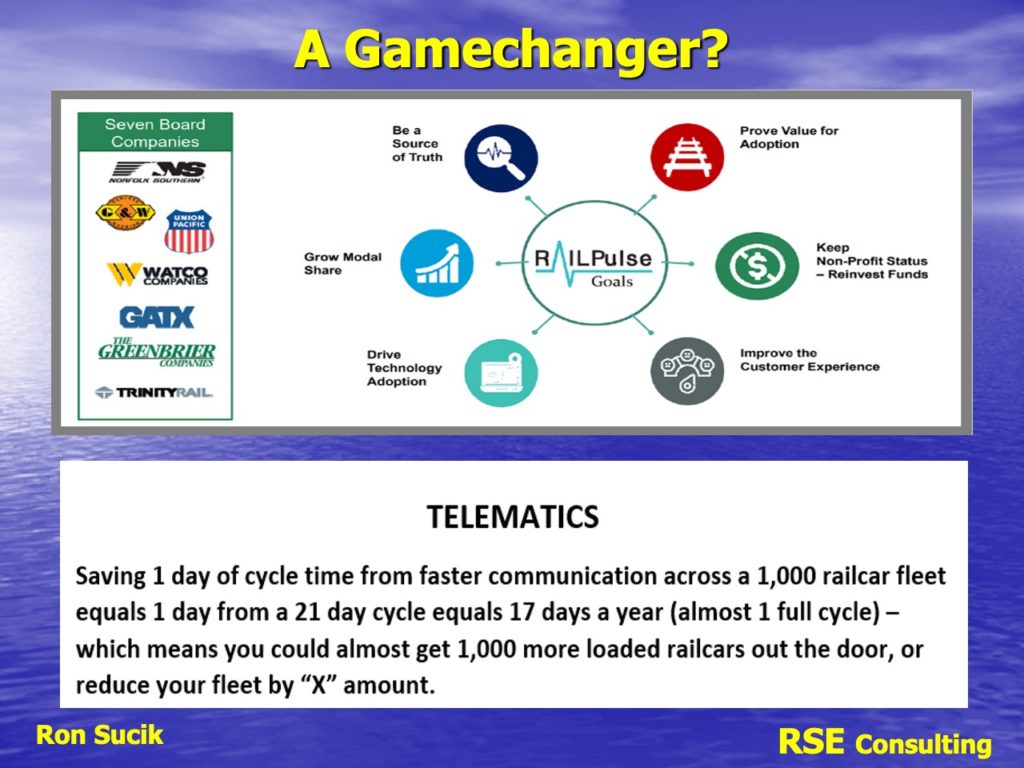

Boston Consulting Group in a recent white paper outlined how RailPulse was formed and what benefits we might expect from the technology. RailPulse is a joint venture of Norfolk Southern, GATX, WATCO, Union Pacific, Trinity Rail, Genesee & Wyoming Inc., The Greenbrier Companies and Railroad Development Corporation.

The adoption of advanced tracking devices known as telematics has the potential to produce vast amounts of data on railcar location, condition and health. Applying this data to improve the customer experience will help the rail industry grow its freight volumes after a decade-long decline in market share.

There will be five major sources of value derived from this data collection:

- Customer Satisfaction and Growth.

- Asset Productivity and Fleet Size.

- Asset and Activity Accounting.

- Automation.

- Asset Health and Safety.

It has been suggested there could be an 8%-plus increase in productivity resulting in higher customer satisfaction and ultimately reduced expenses of maintenance or even fleet ownership. Device testing and application is currently being tested on some Trinity equipment, and you can expect further information as they are completed later this year.

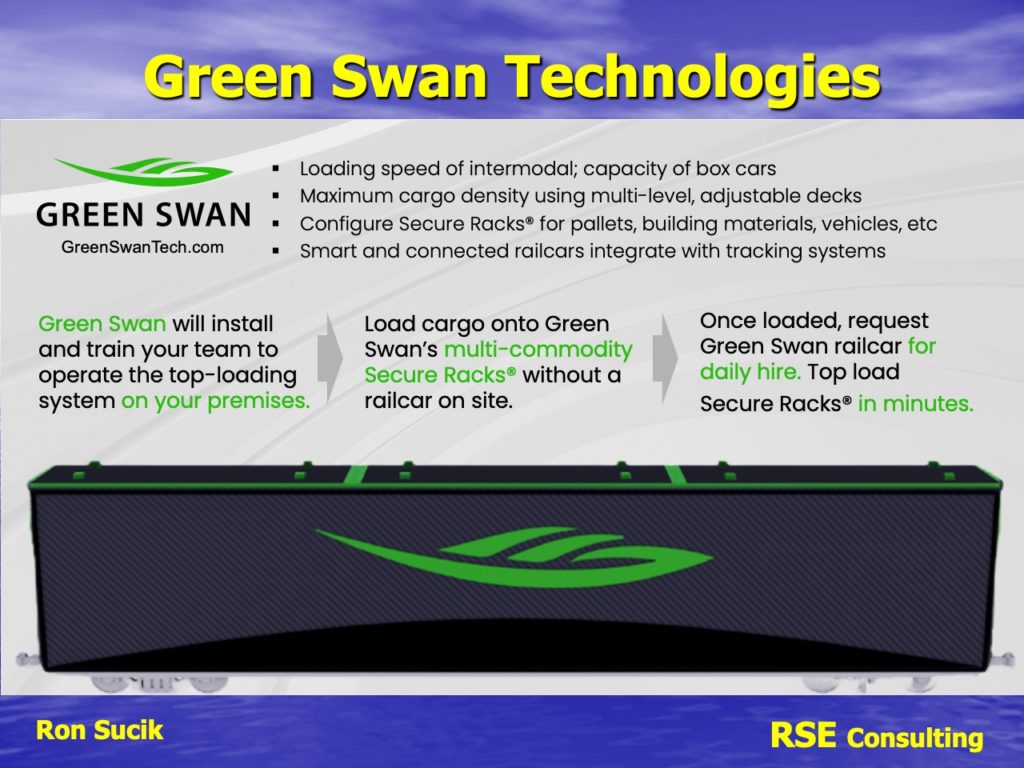

Green Swan Technologies (www.greenswantech.com) has developed a loading system that can help shippers and transloaders convert truck traffic to rail. This technology, invented by an industry outsider, has the potential to be a paradigm shift. It is applicable to many types of cargo, from lumber to palletized goods, because the internal rack changes for the commodity, while the railcar stays the same.

The 60-foot cars are like a well car with sides. The railcar’s roof is attached to the rack, which seals the railcar when loaded through the top. There are no doors, and everything is monitored by onboard sensors and computers. The first production run is expected to be for about 200 cars and 600 racks, which a client is expecting to use to transfer 50 long-haul trucks to rail, per day. The loading technology will be available to everyone, and Green Swan Technologies is looking for transload operators who would like to be early adopters while they build out the fleet. Watch for updates as the first cars are built and put into service.

A couple days ago I spoke with Chris Chase from the POLA (Port of Los Angeles), who had just returned from RILA (Retail Industry Leaders of America) and TPM (Transpacific Maritime Conference). The POLA macro perspective is that the first quarter of 2023 will be soft—what some might call a minor recession—but gradually recover during the second quarter and be more traditional. And by traditional, they mean 2017-2019, not 2020-2021 or 2021-2022.

From RILA: Inventory will work off in 4-5 months and some 90-days-out orders have been placed. Clothing will lead the way as back-to-school items come out during the spring months. This always gives them a bump in the spring. Furniture and larger consumer items will lag and take longer to clear the warehouses.

From TPM: Retailers have experienced major manufacturing shutdowns for three months in China. They are seeing sourcing shifting to Vietnam and Malaysia, especially because they can avoid the tariffs against China. But China has the capacity to fill any size order quickly. Near-shoring works fine for the larger high-end items, but not the low-priced items.

While we hope for a recovery in the second half, intermodal loadings will be fighting an accumulation of situations and events that could make it unlikely. Clothing inventories will correct themselves before the other items and products. Back-to-school products will give intermodal a small bump, but inflation and cost of living is likely to dampen remaining products.

The continued shift of imports away from China and the transition of container movements to East Coast and Gulf ports will dampen demand for rail intermodal moves on the shorter lanes. Additional domestic containers will chase the traffic, and thanks to TTX’s order of additional well cars, there is plenty of equipment to handle any intermodal growth should it occur. I’m doubtful about any intermodal growth in 2023, and anticipate a flat year—but would be very pleased for even 1%.

Ron Sucik is retired from the TTX Business and Market Planning Department but maintains his contacts with all elements of the rail intermodal industry. Ron offers his perspective to entities wishing to understand more about Intermodal and continues to present the intermodal situation at the annual Rail Equipment Finance Conference in La Quinta, Calif.