NS 3Q22: Record Quarterly Results, Improved Service Levels (UPDATED, Cowen)

Written by Carolina Worrell, Senior Editor

NS achieved "record financial results and improved service levels for customers" in third-quarter 2022, President and CEO Alan Shaw said on Oct. 26.

Through its “robust hiring initiatives and the launch and execution of its new operating plan, TOP|SPG,” Norfolk Southern (NS) achieved “record financial results and improved service levels for its customers” in third-quarter 2022, said President and CEO Alan Shaw during an Oct. 26 announcement.

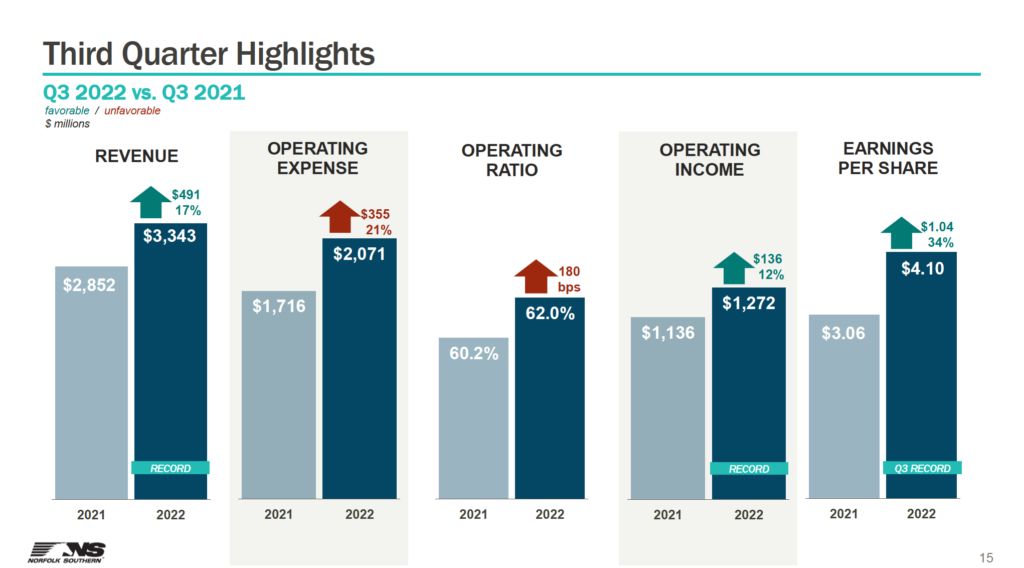

For the three months ended Sept. 30, NS posted railway operating revenues of $3.3 billion, up 17%, or $491 million, compared with the prior-year period, which the railroad attributed to a 20% increase in revenue per unit due to higher fuel surcharges and pricing.

Other third-quarter 2022 highlights:

- Net income was $958 million, up 27% from the $754 million posted in third-quarter 2021.

- Diluted earnings per share came in at $4.10 vs. the prior-year period’s $3.06. “Diluted earnings per share included a $0.28 impact from the wage accruals pertaining to a prior period and a $0.58 benefit from a state tax law change,” NS reported.

- Income from railway operations was a record $1.3 billion, up 12%, or $136 million, and the railway operating ratio was 62.0%, up 180 basis points over third-quarter 2021. “Income from railway operations and the operating ratio were adversely impacted by $88 million and 270 basis points, respectively, compared to the same period prior year due to the wage accruals for prior periods,” NS reported.

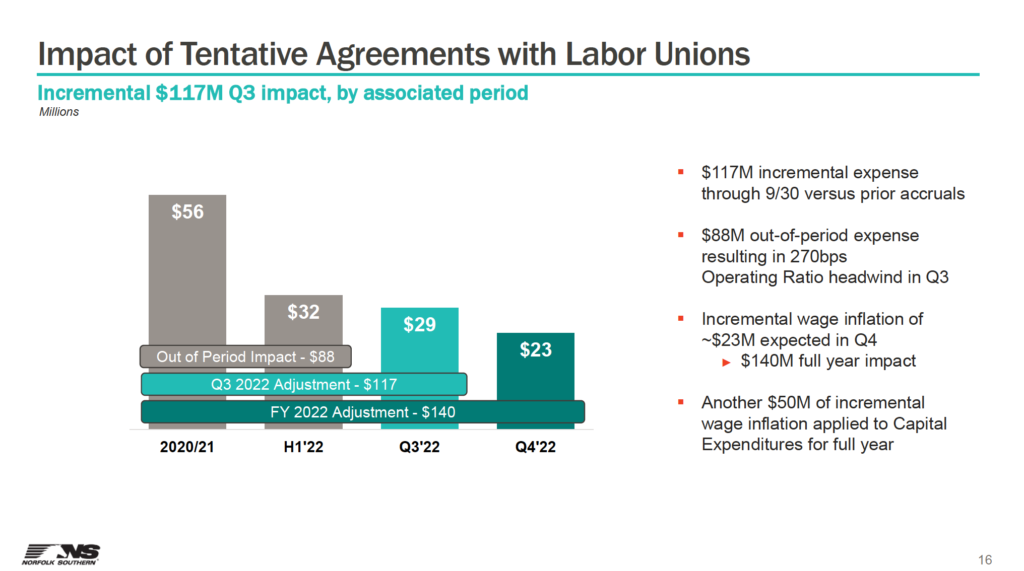

- Railway operating expenses were $2.1 billion, an increase of 21%, or $355 million, compared with the same period last year due to “higher fuel prices, increased labor costs, and other elevated expenses resulting from inflation and slower network velocity,” the railroad reported. “Incremental labor costs of $117 million associated with the terms of the tentative labor agreement were recorded in the quarter, including $88 million in costs pertaining to prior periods,” NS added.

2022 Outlook

Looking ahead, NS reported that for revenue, it expects a year-over-year growth of greater than 13%. Capex is slated to reach between $1.8 billion and $1.9 billion.

“Our entire team is aligned to building on this operational momentum, while ensuring customers remain at the center of our approach, all to deliver value to our shareholders,” Shaw said.

The NS Investor Relations page provides more details.

The Cowen Insight: ‘Network Fluidity Improving But Not There Yet’

“NS reported a mixed quarter with earnings missing our forecast that included tax benefits, labor accruals and legal settlements; incremental wage accruals will be recognized in Q4 and as labor pressure will likely impact OR in 2023,” reported Cowen and Company Managing Director and Railway Age Wall Street Contributing Editor Jason Seidl. “A large question will be NS’s ability to capture intermodal traffic that have been lost due to labor/network challenges. Price target to $243.”

Key Cowen Takeaways:

- “3Q reported EPS of $4.10 was above consensus of $3.64 and our estimate of $3.58 aided by a state tax law change that added $0.58 to the bottom line. Excluding the tax tailwind, the EPS figure comes to $3.52, below our estimate. Wage accruals resulting from tentative agreements with labor unions generated a $0.28 hit to the bottom and a 270bps hit to OR bringing it below our expectations to 62%; we did not exclude the labor accruals in our model. The OR figure also includes a 50bps tailwind from legal settlements.”

- “The labor dispute weighed on NSC’s 3Q results. NSC expects ~$23MM in incremental wage inflation in 4Q, bringing the full year impact of the labor negotiations to $140MM. Management noted that the expense from labor negotiations was about 2x expectation and will generate a ~110bps OR degradation in ’22 compared to expectations. We model as such and worsen our ’23 OR assumptions to reflect the persistence of this wage inflation. The scare of a rail strike also impacted Sept volumes as hazardous material and intermodal shipments were embargoed. Per management, 40-50% of volume decline in 3Q was attributable to embargoes and cost $20-25MM in revenue.”

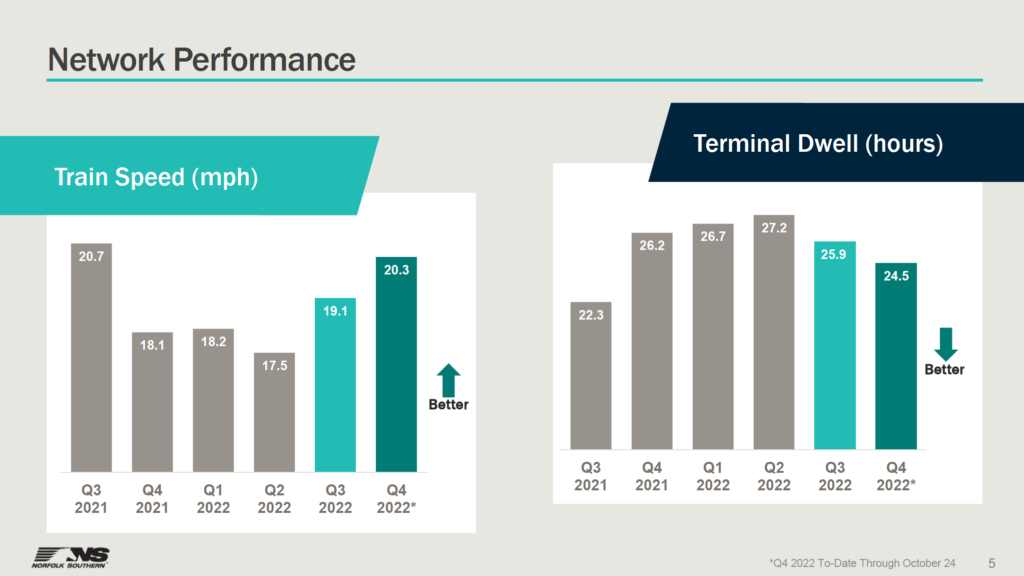

- “There was some decidedly good news in the quarter as it pertained to the company’s operational fluidity. Velocity improved 20% sequentially in the quarter, and NSC attributes TOP SPG for its service recovery, which is trending above the STB’s schedule. That said, volumes still were below expectations in the quarter, and QTD volumes (-2.7%) are below the U.S. carrier average – we look for the service improvements to flow through to volumes but model a sequential step down in total carloadings given clear pockets of softness, most notably intermodal due to weak peak season and persistent chassis shortages. We expect macro pressure on volumes to persist into ’23 despite pockets of strength in coal and autos.”

- “Yields were robust in 3Q across the board growing 20% y/y and supported revenues, aided by fuel surcharges that are expected to normalize in 4Q. Management expressed confidence in core pricing (we expect reported yields to decline somewhat due to the pass-through on coal contracts) in 4Q and we take up our assumptions to reflect this strength. Nonetheless, we see pressure on pricing in ’23 and adjust our yield estimates downward.”